Të dhënat po ngarkohen...

Updated; 10-05-2013, 11:31

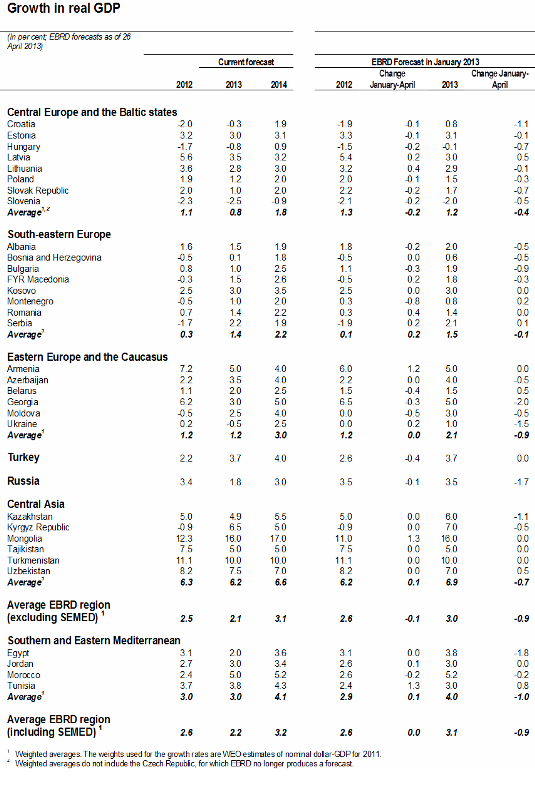

Diminishing impact of Eurozone crisis overshadowed by weakness in Russia and other large economies – structural reforms urgently needed The EBRD has published its latest Regional Economic Prospects report, which contains new forecasts for the transition region. See below, overview of highlights from the report. Summary of key points: • 2013 GDP growth forecast for whole EBRD region revised down sharply to 2.2 % (versus 3.1 % forecast in January (2012 +2.6/2014 +3.2) • Downward revision reflects significant slowdown in growth in Russia, as well other large economies such as Poland and Turkey. • Revision comes even though the effects of the Eurozone crisis on the transition region appear to be abating, with exports recovering and milder cross-border deleveraging. • “A resumption of structural reforms is now urgently needed to pave the way for more robust growth in the future.” Comments from EBRD Chief Economist Erik Berglof: “The reasons for the slowdown in growth differ from country to country, but it should be a wakeup call across the region to reenergise structural reforms – reforms which have been on hold since before the global crisis.” Erik Berglof on the debate of “growth versus austerity”: “This trade-off is not the main issue in our region. Fiscal responsibility is of course important. But most of our countries have already made significant progress in this area during the crisis. What is urgently important now is to advance structural reforms."

Diminishing impact of the Eurozone crisis: • Recent improvement in exports from the CEB and SEE region suggests the negative impact of the Eurozone debt crisis may be lessening. • Cross-border deleveraging has abated overall but this has not yet translated into a clear improvement of credit conditions in countries exposed to the Eurozone • The region will continue to operate in a weak external environment driven by the Eurozone crisis and the resulting mild recession in the single currency area. • The EBRD’s baseline scenario assumes continued slow and uneven progress towards containment of the Eurozone crisis • A possible further deterioration of the Eurozone crisis still poses the largest downside risk to the outlook. New use of unconventional policies Several countries have started experimenting with unconventional demand-boosting measures, either through off-budget funds (e.g. Poland) or unorthodox monetary schemes to support SME lending (e.g. Hungary).. The report says: “Their effectiveness will depend, among others, on good institutional setups as well as removing any other major policy obstacles in the way of recovery.”

Regional highlights: Russia will experience a sharp slowdown with growth of 1.8 % in 2013 and 3.0 % in 2014 after 3.4 % in 2012. The slowdown reflects: • Lower global demand, leading to stagnating commodity prices and export revenues • A slowdown in public social spending growth following last year’s elections • Possible dents to investor confidence following setbacks with business environment reforms and the treatment of foreign investors • Supply side bottlenecks, reflecting record high employment and capacity utilisation in manufacturing Policy options in Russia: Limited prospects for substantial fiscal loosening given official commitment to fiscal rule Some scope for monetary loosening even within the current inflation targeting framework “The most effective way to stimulate growth is to speed up reforms to radically improve the business environment and the investment climate, particularly for foreign investors.”

Central Europe and the Baltics (includes Slovenia and Croatia) Divergent growth patterns: • The Baltic states are all growing strongly – growth close to or above 3% in 2013/2014 • Growth in Poland and the Slovak Republic has slowed sharply • Hungary, Slovenia and Croatia remain mired in recession

In Poland GDP growth is seen slowing to 1.2 % in 2013 (2012 +1.9%; 2014 +2.0) Poland’s resilience to the European recession in 2009, and elevated growth rates of over 4 % in 2010-11, were due to a number of transient factors, including the rapid absorption of EU structural funds and the ensuing boom in public investment The Baltic economies are reaping the benefits of the drastic adjustment in their economies following the output collapse in 2009/10 In Slovenia the recession is set to continue throughout this year as the severe crisis of the banking and corporate sector persists. Croatia continues to be in recession. An acceleration of reforms is needed to benefit fully from EU membership.

South-eastern Europe continues to face serious economic difficulties and risks. Overall, the region recorded only minimal growth in 2012. Prospects for 2013 are slightly better, but there are no major internal or external growth drivers for growth at present. Growth in south-eastern Europe will reach a modest 1.4 % this year and 2.2 % next year, although from a very low 0.3 % last year. Reform efforts in this region have been hesitant and constrained by the difficult economic environment. It remains vulnerable to weaknesses in the Eurozone, the main export market.

Turkey – After a strong performance in 2010 and 2011, the Turkish economy slowed down significantly in 2012 because of weak domestic demand and manufacturing activity coupled with a large drop in the private sector’s capital investments. Growth in 2013 is seen at 3.7 % (4.0 % in 2014), but macroeconomic risks remain. Imports have visibly picked up in the first few months of this year, while exports have slowed down, and the current account deficit has widened again in the first two months of 2013. Most importantly, funding remains relatively short-term and dependent on portfolio flows, which are vulnerable to shifts in global market sentiments.

In Eastern Europe and the Caucasus, the economy in Ukraine is very much exposed to developments in the Eurozone and Russia. The slowdown in both will continue to negatively affect the country’s growth and economic stability. The virtual stagnation in Ukraine in 2012 (+0.2) will likely give way to a small contraction (-0.5) in 2013, with growth seen again in 2014 (+2.5). The Ukrainian economy is running a substantial external deficit, which may require devaluation.

In most of Central Asia, economic growth continued decelerating in response to the global economic slowdown. The deepening slowdown in Russia may have a further negative impact on growth in this region, mainly through the impact on remittance flows, which have so far performed strongly. Mongolia is still growing strongly with expansion of 16% in 2013 and a higher 17% in 2014.

Economic growth momentum has slowed down across the southern and eastern Mediterranean (SEMED) countries, while unemployment, especially among the youth, remains a chronic problem in all four countries and remained persistently high in 2012. In Egypt and Tunisia, volatile political and security conditions have weighed on the economy, adversely affecting investor confidence. Morocco and Jordan have faced weak external conditions and high commodity prices. The SEMED region is likely to expand this year at the same rate as in 2012 (+3.0), but growth is projected to pick up in 2014 (+4.1). In Egypt, growth is seen slowing to +2.0 in 2013 from +3.1 in 2012 While all SEMED countries remain vulnerable to external shocks, Morocco is expected to grow at 5 % in 2013 thanks to a rebound in agricultural production. While the IMF programmes currently in place in Morocco, Tunisia, and Jordan will help investor confidence and buffer against external shocks, a loan agreement with Egypt is still under negotiation. Reaching an agreement could help cement necessary structural reforms and unlock needed external assistance.